HELOC vs Home Equity Loan: Which Is Better for Homeowners?

If you own a home, you may be sitting on one of the most powerful financial tools available: your home equity.

Many homeowners today have hundreds of thousands of dollars in equity but aren’t sure how to access it wisely.

Two of the most common ways to unlock that equity are:

HELOC (Home Equity Line of Credit)

Home Equity Loan

Both allow you to borrow against the value of your home, but they work very differently. Understanding the difference can help you choose the right strategy for renovations, investments, or financial flexibility.

What Is Home Equity?

Home equity is simply the difference between your home's value and what you owe on your mortgage.

Example:

Home value: $1,000,000

Mortgage balance: $600,000

Your equity = $400,000

Most lenders will allow homeowners to borrow up to 80–85% of their home's value, depending on qualifications.

That means in this example you could potentially access $200,000–$250,000 of liquidity.

What Is a HELOC?

A HELOC (Home Equity Line of Credit) works like a credit card secured by your home.

Instead of receiving a lump sum, the lender approves you for a credit line that you can borrow from whenever you need it.

For example:

If you are approved for a $250,000 HELOC, you might:

Borrow $20,000 for a renovation

Borrow another $30,000 later

Pay some of it back

Borrow again if needed

You only pay interest on the amount you actually use.

Most HELOCs have two phases:

Draw Period (typically 10 years)

You can borrow as needed and often make interest-only payments.Repayment Period (10–20 years)

Borrowing stops and you begin paying principal and interest.

Advantages of a HELOC

Flexible access to funds

Interest charged only on the amount used

Useful for renovations or projects with uncertain costs

Can serve as a financial safety net or liquidity line

Potential Downsides of a HELOC

Most HELOC rates are variable

Payments can increase if interest rates rise

Requires discipline to avoid overspending

What Is a Home Equity Loan?

A Home Equity Loan is sometimes called a second mortgage.

Instead of a credit line, the lender provides one lump sum upfront, and you repay it with fixed monthly payments over time.

Example:

Loan amount: $100,000

Interest rate: 7% fixed

Term: 20 years

Your payment remains predictable and fixed for the life of the loan.

Advantages of a Home Equity Loan

Fixed interest rate

Stable monthly payment

Ideal for large known expenses

Examples include:

Major home renovations

Debt consolidation

Large one-time purchases

Downsides of a Home Equity Loan

Less flexible than a HELOC

Interest begins on the entire loan immediately

Funds cannot be re-borrowed once paid down

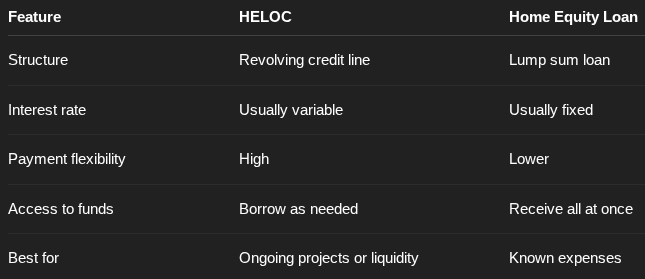

HELOC vs Home Equity Loan (Quick Comparison)

Which Option Is Right for You?

A HELOC may be best if you:

Plan to renovate over time

Want a liquidity safety net

Prefer borrowing only what you need

Value flexibility

A Home Equity Loan may be better if you:

Need a specific amount of money upfront

Want predictable fixed payments

Prefer protection from rising interest rates

A Strategy Many Homeowners Use

Even homeowners who don’t currently need funds sometimes open a HELOC as a financial backup plan.

Why?

Because once approved, it gives them access to liquidity when opportunities or emergencies arise.

Think of it as a financial safety net attached to your home equity.

Curious How Much Equity You Could Access?

Every homeowner’s situation is different. Loan limits depend on:

Home value

Current mortgage balance

Credit profile

Income and debt levels

If you’d like to explore your options, I’m happy to help.

As a mortgage advisor, I work with multiple wholesale lenders to help homeowners find the most competitive equity financing solutions available.

Request a Free Home Equity Consultation

If you're considering tapping into your home equity, I can help you:

Estimate how much equity you can access

Compare HELOC vs home equity loan options

Evaluate rates and lender programs

Structure the best solution for your goals

Schedule a consultation or feel free to reach out directly.

The right equity strategy can turn your home into a powerful financial tool.